Howard Marks did not build a highly successful money management firm (Oaktree Capital) by ignoring the fundamental truths and the basic laws of economics. In his latest memo, "Economic Reality," he explains simply and eloquently why it is that a) monetary policy cannot stimulate an economy or create growth, b) governments cannot create growth by subsidizing industries, c) government regulations (e.g., minimum wage laws) cannot produce prosperity, d) higher taxes on the rich cannot make an economy stronger or increase the general welfare of a country's citizens, e) higher inflation mainly benefits governments with big debts, at the expense of its citizens, f) devaluing one's currency cannot strengthen an economy, g) bringing jobs back to the U.S. is not necessarily going to raise our standard of living (and Trump's promise to impose huge tariffs on Chinese goods is crazy), and h) redistributing wealth and central planning are sure-fire ways to destroy an economy.

I highly recommend this memo to everyone. It's long, but chock-full of wisdom that is sorely needed (and distressingly lacking) in today's political debates.

Tuesday, May 31, 2016

Wednesday, May 25, 2016

Risk aversion is still the order of the day

The S&P 500 is only 2% away from making a new, all-time high, and its PE ratio today of 19.3 (according to Bloomberg) is about 15% above its 55-yr average. The Fed has been taking extraordinary measures to ensure that the economy has plenty of liquidity, and has targeted extremely low short-term interest rates for over 7 years. Taking these facts into consideration, you could be forgiven for thinking that super-easy monetary policy and low interest rates have created another bubble in the price of risk assets.

There is no shortage of pundits, economists, and investors who are worried that the Fed has blown an asset-price bubble that is ready to pop. I'm among the minority who have been arguing—for many years—that this is the wrong way to look at things. I don't see the Fed as the aggressor; I think the Fed is more a follower. The Fed hasn't driven yields to absurdly low levels, the Fed has merely responded to a market that has been deeply risk averse and generally pessimistic.

The Fed has been doing what it should: in the presence of a huge demand for money and safe assets, the Fed must take extraordinary measures to increase the supply of money and safe assets. Quantitative Easing was not money printing. It was the Fed's way of turning risky notes and bonds into safe assets (i.e., bank reserves, which are functionally equivalent to T-bills, the gold standard of risk-free assets). The demand for money and safe assets has been unprecedented, and the Fed's response has been commensurate. I explained this in greater detail here.

Evidence of risk aversion (another way of describing the market's huge demand for money and safe assets) is everywhere. Investors all over the globe are willing to pay extremely high prices for risk-free assets, while at the same time shunning much higher yields on risk assets. Moreover, it's not unreasonable for there to be so much risk aversion: economic growth has been miserably slow just about everywhere, and volatility has at times been intense. Most people are still terrified of another Great Recession and/or Global Financial Market Crash. Once burned, twice shy, as the saying goes.

Here are a bunch of charts, in no particular order, which help prove my points:

Households have reacted to the Great Recession by cleaning up their balance sheets. As the chart above shows, financial obligations as a % of disposable income are now at multi-decade lows. Households have almost never been so prudent in managing their finances. Nobody wants to get caught with too much debt when/if the next financial crisis rolls around.

Leverage was all the rage in the 2000s, as home prices escalated and mortgages became easier to find and abuse. But the housing market collapse taught us all a valuable and time-honored lesson: prices can't go up forever, even if money is almost free. As a result, the average person is far less leveraged today than he or she was a decade ago, as the chart above shows.

You know things are getting shaky when delinquency rates on loans start rising, because that is evidence that borrowers are getting stretched. Today that's not the case at all. In fact, as the chart above shows, delinquency rates on consumer loans and credit cards have never been lower. People have learned the hard way that leverage doesn't always pay.

People have also learned that credit card debt is a killer. As the chart above shows, outstanding credit card debt today is still far less than it was in 2008, and as a % of disposable income, credit card debt has collapsed, and hasn't risen at all for the past several years.

The chart above is the quintessential measure of the demand for money. It shows the ratio of M2 (currency, checking accounts, CDs,consumer savings deposits and retail money market funds, all very liquid and spendable forms of money) to nominal GDP. The ratio has never been higher, and it has been rising by leaps and bounds for the past 15 years. This tells us that people want to hold an ever-increasing amount of their annual income in the form of money and money equivalents. Bank savings deposits, for example, have risen from $4 trillion in late 2008 to $8.4 trillion today (a 110% increase); over the same period, personal income has risen by a mere 27%. People have been actively socking away money like squirrels before the winter arrives. Virtually the entire avalanche of new bank savings deposits has been used by banks to buy notes and bonds which in turn they sold to the Fed in exchange for bank reserves. The banking system, in other words, invested their huge deposit inflows in the safest thing they could find: T-bill equivalents (aka bank reserves). Bank credit is growing at a 7-8% rate, but that is only a very small fraction of what it could be, given the huge amount of excess reserves that banks hold. Banks are behaving just like people who are very risk averse.

U.S. Treasury notes and bonds are universally considered to be the safest of all notes and bonds, given the guarantee of the U.S. government. 10-yr Treasury yields, shown in the chart above, today are a mere 1.87%, which is only inches higher than the all-time low of 1.4% registered about four years ago. That's another way of saying that the price of these bonds is very close to an all-time high. People all over the world are willing to pay top dollar for the safety of these bonds relative to other bonds. The PE ratio of the 10-yr Treasury today is about 53: to get a dollar's worth of yield on a 10-yr Treasury you have to pay $53. Compare that to the PE ratio on the average large cap stock today, which is just over 19, and you get a vivid feel for just how risk averse this market is.

In fact, the best measure of bond yields (i.e., their real yields) is the place to start your analysis of the bond market. As the chart above shows, there is a strong tendency for the real yield on 5-yr TIPS to track the real growth rate of the economy. That's not unusual at all. Think of the real yield on 5-yr TIPS as the risk-free expected real yield. It should be lower that the expected real return on riskier assets, just as the yield on T-bills should be lower than the expected nominal yield on riskier assets. (This is straight out of modern finance theory.) You shouldn't be able to lock in a real rate of return that is higher than the expected real rate of return on risky assets; you should almost lways have to pay a premium for the risk-free nature of TIPS. 5-yr TIPS today have a slightly negative real yield, and that implies that the market expects that average real returns on other assets (for which real growth expectations are a good proxy) should be somewhat higher, and indeed they are, but not by much. As the chart above shows, 5-yr TIPS real yields today suggest that the market expects real GDP growth to be about 1-2% per year for the foreseeable future. That's a pretty pessimistic outlook. Real yields are low because nobody's taking the risks that are necessary to generate stronger growth; corporate profits are at near-record levels relative to GDP, but corporate investment is miserably weak. Weak growth implies low real and nominal yields on Treasuries, as long as inflation expectations remain anchored, as they still are.

As the chart above shows, fear has been a huge factor in the stock market for the past several years. I use the ratio of the Vix Index (the implied volatility of equity options, a good measure of fear and uncertainty) to the 10-yr Treasury yield (a good measure of the market's expectations for economic growth, as discussed above) as a measure of how worried and pessimistic the market is. Bouts of nerves and pessimism have driven the market lower repeatedly. Prices have recovered in the past few months as fears of deflation and fears of a China collapsed have receded. But the Vix/10-yr ratio is still elevated, thanks mainly to very low Treasury yields.

Yesterday brought the welcome news of a surge in new home sales in April, as shown in the chart above. There are still bright spots out there, thank goodness.

But as the chart above shows, the housing market is still pretty depressed from an historical perspective, even 10 years after its prior peak. Starts today are only about half what they have been during prior periods of good times.

When markets are risk-averse, as they still are today, investors enjoy a cushion of sorts against bad news, because the existence of risk aversion equates to bad news being priced in.

There is no shortage of pundits, economists, and investors who are worried that the Fed has blown an asset-price bubble that is ready to pop. I'm among the minority who have been arguing—for many years—that this is the wrong way to look at things. I don't see the Fed as the aggressor; I think the Fed is more a follower. The Fed hasn't driven yields to absurdly low levels, the Fed has merely responded to a market that has been deeply risk averse and generally pessimistic.

The Fed has been doing what it should: in the presence of a huge demand for money and safe assets, the Fed must take extraordinary measures to increase the supply of money and safe assets. Quantitative Easing was not money printing. It was the Fed's way of turning risky notes and bonds into safe assets (i.e., bank reserves, which are functionally equivalent to T-bills, the gold standard of risk-free assets). The demand for money and safe assets has been unprecedented, and the Fed's response has been commensurate. I explained this in greater detail here.

Evidence of risk aversion (another way of describing the market's huge demand for money and safe assets) is everywhere. Investors all over the globe are willing to pay extremely high prices for risk-free assets, while at the same time shunning much higher yields on risk assets. Moreover, it's not unreasonable for there to be so much risk aversion: economic growth has been miserably slow just about everywhere, and volatility has at times been intense. Most people are still terrified of another Great Recession and/or Global Financial Market Crash. Once burned, twice shy, as the saying goes.

Here are a bunch of charts, in no particular order, which help prove my points:

Households have reacted to the Great Recession by cleaning up their balance sheets. As the chart above shows, financial obligations as a % of disposable income are now at multi-decade lows. Households have almost never been so prudent in managing their finances. Nobody wants to get caught with too much debt when/if the next financial crisis rolls around.

Leverage was all the rage in the 2000s, as home prices escalated and mortgages became easier to find and abuse. But the housing market collapse taught us all a valuable and time-honored lesson: prices can't go up forever, even if money is almost free. As a result, the average person is far less leveraged today than he or she was a decade ago, as the chart above shows.

You know things are getting shaky when delinquency rates on loans start rising, because that is evidence that borrowers are getting stretched. Today that's not the case at all. In fact, as the chart above shows, delinquency rates on consumer loans and credit cards have never been lower. People have learned the hard way that leverage doesn't always pay.

People have also learned that credit card debt is a killer. As the chart above shows, outstanding credit card debt today is still far less than it was in 2008, and as a % of disposable income, credit card debt has collapsed, and hasn't risen at all for the past several years.

The chart above is the quintessential measure of the demand for money. It shows the ratio of M2 (currency, checking accounts, CDs,consumer savings deposits and retail money market funds, all very liquid and spendable forms of money) to nominal GDP. The ratio has never been higher, and it has been rising by leaps and bounds for the past 15 years. This tells us that people want to hold an ever-increasing amount of their annual income in the form of money and money equivalents. Bank savings deposits, for example, have risen from $4 trillion in late 2008 to $8.4 trillion today (a 110% increase); over the same period, personal income has risen by a mere 27%. People have been actively socking away money like squirrels before the winter arrives. Virtually the entire avalanche of new bank savings deposits has been used by banks to buy notes and bonds which in turn they sold to the Fed in exchange for bank reserves. The banking system, in other words, invested their huge deposit inflows in the safest thing they could find: T-bill equivalents (aka bank reserves). Bank credit is growing at a 7-8% rate, but that is only a very small fraction of what it could be, given the huge amount of excess reserves that banks hold. Banks are behaving just like people who are very risk averse.

The chart above compares the price of gold to the price of 5-yr TIPS (using the inverse of their real yield as a proxy for their price). These are two classic safe assets: gold has been the safe haven asset par excellence for all of history, and 5-yr TIPS are the only way an investor can lock in a guaranteed real rate of interest on an asset that is itself risk-free. Although the prices of gold and TIPS have fallen over the past several years (they peaked around the time of the PIIGS crisis in the Eurozone), they are still quite elevated from an historical perspective. In constant dollar terms, gold prices have averaged $500-600 over the past century, while real yields on 5-yr TIPS have averaged 1.3% since their inception in 1997. Investors are still willing to pay a hefty premium for the safety these two assets afford.

U.S. Treasury notes and bonds are universally considered to be the safest of all notes and bonds, given the guarantee of the U.S. government. 10-yr Treasury yields, shown in the chart above, today are a mere 1.87%, which is only inches higher than the all-time low of 1.4% registered about four years ago. That's another way of saying that the price of these bonds is very close to an all-time high. People all over the world are willing to pay top dollar for the safety of these bonds relative to other bonds. The PE ratio of the 10-yr Treasury today is about 53: to get a dollar's worth of yield on a 10-yr Treasury you have to pay $53. Compare that to the PE ratio on the average large cap stock today, which is just over 19, and you get a vivid feel for just how risk averse this market is.

But hold on, you say; isn't it the case that the Fed has artificially depressed the yield on Treasuries by buying trillions worth of them? Not necessarily, and most likely not. As the chart above shows, the Fed today holds the same percentage of outstanding Treasuries as it did prior to the 2008 financial crisis. And there's little or no correlation between changes in the Fed's relative holdings and the yield on those same Treasuries. For example, look at how the Fed's holdings soared in 2012-2014, at the same time that yields soared. You would have thought that huge Fed purchases would have pushed up Treasury prices and depressed Treasury yields, but just the opposite occurred. I explained this in greater detail here.

My point here is that the Fed cannot distort the yield on notes and bonds. The Fed can exert strong influence on short-term rates, but not on 5- and 10-yr rates. Besides, we have the TIPS market that helps discipline yields. In the chart above, I show the nominal yield on Treasuries and the real yield on their corresponding TIPS (Treasury Inflation-Protected Securities), and the difference, which is the market's implied inflation expectation. We know the Fed has purchased trillions of Treasuries, but they've only purchased about $60 billion of TIPS since 2008 (the Fed held 8.5% of outstanding TIPS as of March 2016). If nominal yields were artificially low because of huge Fed purchases, then the expected inflation rate should have been artificially low as well, but it is today very much in line with current inflation and forward-looking inflation expectations.

In fact, the best measure of bond yields (i.e., their real yields) is the place to start your analysis of the bond market. As the chart above shows, there is a strong tendency for the real yield on 5-yr TIPS to track the real growth rate of the economy. That's not unusual at all. Think of the real yield on 5-yr TIPS as the risk-free expected real yield. It should be lower that the expected real return on riskier assets, just as the yield on T-bills should be lower than the expected nominal yield on riskier assets. (This is straight out of modern finance theory.) You shouldn't be able to lock in a real rate of return that is higher than the expected real rate of return on risky assets; you should almost lways have to pay a premium for the risk-free nature of TIPS. 5-yr TIPS today have a slightly negative real yield, and that implies that the market expects that average real returns on other assets (for which real growth expectations are a good proxy) should be somewhat higher, and indeed they are, but not by much. As the chart above shows, 5-yr TIPS real yields today suggest that the market expects real GDP growth to be about 1-2% per year for the foreseeable future. That's a pretty pessimistic outlook. Real yields are low because nobody's taking the risks that are necessary to generate stronger growth; corporate profits are at near-record levels relative to GDP, but corporate investment is miserably weak. Weak growth implies low real and nominal yields on Treasuries, as long as inflation expectations remain anchored, as they still are.

Risk aversion can be found in the corporate bond market as well. As the chart above shows, credit spreads today are much lower than they were during prior panics, but they are still elevated relative to where they have traded during periods of relative calm.

As the chart above shows, fear has been a huge factor in the stock market for the past several years. I use the ratio of the Vix Index (the implied volatility of equity options, a good measure of fear and uncertainty) to the 10-yr Treasury yield (a good measure of the market's expectations for economic growth, as discussed above) as a measure of how worried and pessimistic the market is. Bouts of nerves and pessimism have driven the market lower repeatedly. Prices have recovered in the past few months as fears of deflation and fears of a China collapsed have receded. But the Vix/10-yr ratio is still elevated, thanks mainly to very low Treasury yields.

Yesterday brought the welcome news of a surge in new home sales in April, as shown in the chart above. There are still bright spots out there, thank goodness.

But as the chart above shows, the housing market is still pretty depressed from an historical perspective, even 10 years after its prior peak. Starts today are only about half what they have been during prior periods of good times.

When markets are risk-averse, as they still are today, investors enjoy a cushion of sorts against bad news, because the existence of risk aversion equates to bad news being priced in.

Tuesday, May 17, 2016

Core inflation is a solid 2%

According to the Ex-Energy version of the Consumer Price Index, inflation has been averaging about 2% per year for well over a decade. Of course, when you add back in energy prices—which have experienced gigantic swings from a low of $10/bbl in 1999 to a high of $150/bbl in 2008, to the current $50/bbl—inflation has been quite volatile. But if ever there were a time to ignore the impact of energy prices on inflation, now is the time. In real terms, oil prices today are only about 10% less than what they have averaged since 1970. So focusing on ex-energy inflation is justified and appropriate, since energy prices have increased by almost the same as all other prices, on average, for the past 45 years. Energy is not noticeably cheap nor expensive relative to other prices these days.

The chart above plots the Ex-Energy version of the CPI on a semi-log scale. It shows that inflation has had a strong tendency to average 2% per year. The only thing unusual about the behavior of inflation was in the 2006-2008 period, when core inflation reached almost 3% and ex-energy inflation slightly exceeded 3%. Since then, and despite massive increases in bank reserves, inflation has been remarkably stable and relatively low.

The chart above draws our attention to the current episode of a major decline in oil prices, and the decline of similar magnitude which occurred in 1986. Both times oil prices plunged, only to later rebound. In 1986 the headline inflation rate collapsed, then returned to the prevailing level of core and ex-energy inflation about a year after oil prices started to rebound. This time should be no different. Today we learned that the CPI increased by 0.4% in April, lifting the year over year rate to 1.1%. If the monthly increases in the CPI are only 0.2% per month for the rest of this year, inflation for 2016 would be 2.0%. That's not difficult to imagine at all.

The Fed is well aware of this dynamic, which is why they haven't panicked over the low rates of headline inflation we have seen over the past year or so. What worries them is that the economy remains sluggish and they know that the market is very nervous about the potential for higher rates to weaken the economy further. I don't think another 25 bps hike in short-term rates would do much harm to the economy, but it's hard to make a compelling argument for doing so. After all, inflation is running right around the Fed's target, and the economy is unlikely to soon defy the myriad headwinds which have been holding it back for the past seven years.

The real action these days is in the election dynamics. The future course of fiscal policy could make a world of difference to the economic outlook in coming years. But for the moment the outcome of the November elections is a jump ball. We'll just have to wait and see how things progress in the months to come. I suspect the Fed will reach the same conclusion and stand pat at the June FOMC meeting four weeks from now.

Thursday, May 12, 2016

The end of declining deficits

On a rolling 12-month basis, the federal budget deficit hit a peak of almost $1.5 trillion in February 2010. From that dizzying height of just over 10% of GDP it fell steadily for six years, hitting a low of $402 billion last February, a mere 2.3% of GDP. It's unlikely to get any lower than that, unfortunately, unless and until we see stronger economic growth and/or significant reform to entitlement programs. For the foreseeable future, the budget deficit is likely to get bigger; it's already jumped to just over $500 billion as of last month. There are several culprits: weaker economic growth, weaker tax collections, and a pickup in spending.

The chart above shows the nominal level of federal spending and revenues on a rolling 12-month basis. Note that spending was flat from mid-2009 through last year, but is now on a clear uptrend. At the same time, it appears that the strong uptrend in tax revenues, from early 2010 through early last year, is fizzling out. Two virtuous trends have reversed.

The chart above shows the level of federal spending and revenues as a percent of GDP. Note how both have been trendless over long periods.

It's time for policymakers to revisit Hauser's Law: there is a limit to how much tax revenue can be extracted from the private sector, and we are now approaching that limit. Tax rates have risen in the past year or so, but tax collections have weakened. Raising taxes—as both Clinton and Sanders are proposing—will almost surely fail to close our current and projected budget gap, because higher rates will discourage work and investment, while encouraging more tax evasion.

As the chart above shows, the weakness in tax collections is concentrated in individual and corporate income tax collections—both of which are driven by weaker profits—while payroll tax collections are rising at a 4% rate that is commensurate with the ongoing rise in payrolls and wages.

The first of the two charts above shows the nominal level of federal budget surpluses and deficits, while the second shows the level as a % of GDP. There's nothing necessarily scary here, since it will be awhile before the deficit rises meaningfully relative to GDP. The larger message is that the budget deficit is going to be returning to the headlines before too long, and politicians who fail to understand Hauser's Law will mistakenly call for a fix in the form of higher tax rates. The correct fix, of course, would be to reduce tax rates, simplify the tax code, and reform entitlement programs in order to keep spending under control.

Friday, May 6, 2016

April jobs report: more of the same

The April jobs report was weaker than expected (160K vs. 200K), but from a big-picture perspective it was no different than what we've been seeing for the past several years. Private sector jobs—the ones that count—have been growing a little more than 2% per year since mid-2011. Add some meager productivity to that number, and it's reasonable to assume that the economy is still growing at a 2 - 2 ½% annual pace. In other words, the weakest recovery in modern times continues.

As the charts above show, April's "weak" jobs growth was par for the course. The jobs number is naturally volatile from month to month. So it's best to look at the change over several months or even a year. On a year over year basis, private sector jobs rose 2.2%; over the past six months, they are up at a 2.1% rate, which is about what they have averaged since mid-2011. Nothing much has changed.

What has changed is the growth of the labor force, which has picked up of late. That explains why the unemployment rate has stopped declining: on the margin, more people are deciding they want to work. This is a positive development.

It's also encouraging that the growth of public sector jobs has on balance been zero for almost 10 years. The physical size of the public sector has been shrinking relative to the private sector, and that makes it easier for private initiative to take root.

In any event, what this means is that the weak GDP growth numbers of the past two quarters are an anomaly that should be reversed via higher numbers over the remainder of this year.

As the charts above show, April's "weak" jobs growth was par for the course. The jobs number is naturally volatile from month to month. So it's best to look at the change over several months or even a year. On a year over year basis, private sector jobs rose 2.2%; over the past six months, they are up at a 2.1% rate, which is about what they have averaged since mid-2011. Nothing much has changed.

What has changed is the growth of the labor force, which has picked up of late. That explains why the unemployment rate has stopped declining: on the margin, more people are deciding they want to work. This is a positive development.

It's also encouraging that the growth of public sector jobs has on balance been zero for almost 10 years. The physical size of the public sector has been shrinking relative to the private sector, and that makes it easier for private initiative to take root.

In any event, what this means is that the weak GDP growth numbers of the past two quarters are an anomaly that should be reversed via higher numbers over the remainder of this year.

Wednesday, May 4, 2016

Productivity is still the missing ingredient

This is a re-posting, with updated data and commentary, of a similar post three months ago.

We've know for years that this recovery is the weakest post-war recovery on record, and the chart above makes the case. If this had been a typical recovery, national income (GDP) would be about $2.8 trillion higher than it is today. That's like saying that average wages and salaries would be 17% higher. For a family earning $60,000, that's over $10,000 more income per year that has failed to materialize despite all their hard efforts.

What's been lacking is productivity (the additional output that each unit of labor produces), because productivity is the key to rising prosperity. We can only earn more if we work and/or produce more. We've had about the same rate of jobs growth (~2%) during this recovery as we had in the latter portion of the 2001-2007 recovery, but GDP growth has been much weaker. The reason? Very low productivity growth, as seen in the chart above. I use a 2-yr rolling annualized growth rate to measure productivity, since it is quite volatile on a quarter-to-quarter basis. Over a 2-year period I think the quarterly volatility tends to wash out and a truer picture is revealed. Note that the productivity readings we've had in the past several years have always been associated in the past with recessions. It's no wonder that everyone keeps complaining about the economy. It's as if we've been living in recessionary conditions even though things have been slowly improving. Put another way, we've had to work unusually hard just to enjoy very modest improvements in our standard of living.

The chart above uses the same data, but instead of a two-year rolling period, it uses a 5-yr rolling period. This, I believe, captures the effect of policies put in place by different presidential administrations. It can take years for policies to be put into effect and then have an impact on the economy, and good policies can have effects that last even after they have been reversed.

The colored bars correspond to different presidential terms, with the red bars reflecting a sustained period of declining productivity growth and the green bars a sustained period of very strong and/or rising productivity growth. I would be quick to note that Republican administrations have yielded three periods of declining productivity (Eisenhower, Nixon, and Bush II), while Democratic administrations have only yielded two periods of declining productivity (Carter and Obama). No political party can lay a claim to implementing policies that consistently lead to sustained rises in prosperity.

One thing that stands out is that the Obama years have seen productivity growth that rivals the malaise that characterized the Carter administration. For the five- and six-year periods ending last March, non-farm productivity rose at a miserably slow 0.5% annualized rate. In all of post-war history, only the five-year period ending in mid-1982 was worse. (Small footnote: Reagan's announced tax cuts did not take effect for almost two years, so his faulty implementation of tax cuts—which encouraged people to delay investments—only served to prolong the declining productivity of the Carter years).

There are many factors that contribute to the slow growth of productivity, such as rising regulatory burdens that increase the cost of economic activity, high marginal tax rates that reduce the incentive to work and invest and take risk, and transfer payments that create a culture of dependency and a reluctance to seek out work. John Cochrane has an excellent op-ed in the WSJ which expands on the reasons why this has been such a weak recovery: "Ending America's Slow-Growth Tailspin."

The charts above show that a significant increase in transfer payments (money the government gives to people for a variety of reasons) beginning in late 2008 corresponded to the beginnings of a significant decline in the labor force participation rate. Many millions of workers have left the workforce, and it could be due at least in part to the fact that the benefits that accrue to those not working (e.g., food stamps, disability payments, welfare, earned income credits, assistance to single-parent families) are greater than the net benefits of working, especially on an after-tax basis. Transfer payments now equal 20% of disposable income, and that is a big number that currently totals $2.74 trillion and consumes fully 73% of all federal government spending. Maybe it's simply the case that our government has grown to the point where it is now suffocating the private sector. Too few people are working and too many are on the receiving end of federal largesse. And for those who are still working, the burden of complying with regulations and the burden of taxes is inhibiting their ability and willingness to work and invest more.

We are not going to see significant improvement in productivity and living standards unless and until we adopt policies that are more conducive to work, investment, and risk-taking. It's that simple. Unfortunately, the proposals being discussed on the left (e.g., higher taxes on income and capital, plus higher minimum wages which price many young workers out of the market and inhibit new business formation) are only going to exacerbate the current situation. Trump sensibly advocates for lower and simpler income and business tax regimes, but his calls for trade protection are misguided and could weaken the economy.

One thing that stands out is that the Obama years have seen productivity growth that rivals the malaise that characterized the Carter administration. For the five- and six-year periods ending last March, non-farm productivity rose at a miserably slow 0.5% annualized rate. In all of post-war history, only the five-year period ending in mid-1982 was worse. (Small footnote: Reagan's announced tax cuts did not take effect for almost two years, so his faulty implementation of tax cuts—which encouraged people to delay investments—only served to prolong the declining productivity of the Carter years).

There are many factors that contribute to the slow growth of productivity, such as rising regulatory burdens that increase the cost of economic activity, high marginal tax rates that reduce the incentive to work and invest and take risk, and transfer payments that create a culture of dependency and a reluctance to seek out work. John Cochrane has an excellent op-ed in the WSJ which expands on the reasons why this has been such a weak recovery: "Ending America's Slow-Growth Tailspin."

We are not going to see significant improvement in productivity and living standards unless and until we adopt policies that are more conducive to work, investment, and risk-taking. It's that simple. Unfortunately, the proposals being discussed on the left (e.g., higher taxes on income and capital, plus higher minimum wages which price many young workers out of the market and inhibit new business formation) are only going to exacerbate the current situation. Trump sensibly advocates for lower and simpler income and business tax regimes, but his calls for trade protection are misguided and could weaken the economy.

Yesterday the level of uncertainty surrounding this year's presidential election was reduced as Trump became the presumptive Republican nominee. But uncertainty remains inordinately high since future policies could take either a positive or a negative direction, and by a lot, regardless of who wins. We know one of the eventual two candidates, but Hillary's candidacy remains deeply clouded by the ongoing FBI investigations. Such a level of uncertainty is not conducive to new investment and is not likely to be inflating equity prices—small comfort.

UPDATE: There is school of thought that holds that the productivity slowdown is the result of mismeasurement; that many valuable products (e.g., GPS, VoIP) are being given away for free. Here is a paper that considers whether this argument is supported by the facts. It concludes: " the reasonable prima facie case for the mismeasurement hypothesis faces real hurdles when confronted with the data." In other words, mismeasurement problems can't come close to explaining the magnitude of the decline in productivity. (HT: John Cochrane)

UPDATE: There is school of thought that holds that the productivity slowdown is the result of mismeasurement; that many valuable products (e.g., GPS, VoIP) are being given away for free. Here is a paper that considers whether this argument is supported by the facts. It concludes: " the reasonable prima facie case for the mismeasurement hypothesis faces real hurdles when confronted with the data." In other words, mismeasurement problems can't come close to explaining the magnitude of the decline in productivity. (HT: John Cochrane)

Healthy service sector

The April ISM service sector report was uniformly healthy. The composite reading was a bit above expectations (55.7 vs. 54.8), and solidly in expansion territory. The service sector is home to some 70% of U.S. payrolls, so this is very good news. The mini-slump that so worried markets earlier this year appears to have faded away.

Both the services and the manufacturing ISM indices confirmed that activity picked up towards the end of the first quarter, all but erasing the earlier slump. This likely means that the economy is back on the 2% growth track that has prevailed for the duration of the current business cycle expansion.

The U.S. and Eurozone economies have been tracking each other for the past 3-4 years, with both growing moderately.

The chart above compares the growth of prices in the service, non-durable, and durable goods sectors. Since 71% of the US workforce is employed in the private service sector, and since the cost of services is largely determined by wages, we can infer that the vast majority of the US workforce has been enjoying very healthy wage gains relative to durable goods prices. Service sector prices have been increasing at a modest 2% annual rate for the past several years, but they have increased two and a half times faster than durable goods prices since 1995 (which happens to mark the start of China's huge export boom).

This is equivalent to saying that an hour's worth of work in the service sector buys 2.5 times as much in the way of durable goods as it did in 1995. We can lament the tepid growth in median incomes over the past few decades, but this significantly understates the gains in workers' purchasing power for durable goods. Practically anyone who works these days is able to afford a smartphone, a device that replaces goods that would have cost a small fortune just 20 years ago. Let's not lose our perspective: things could be a lot better, but they could also be a lot worse.

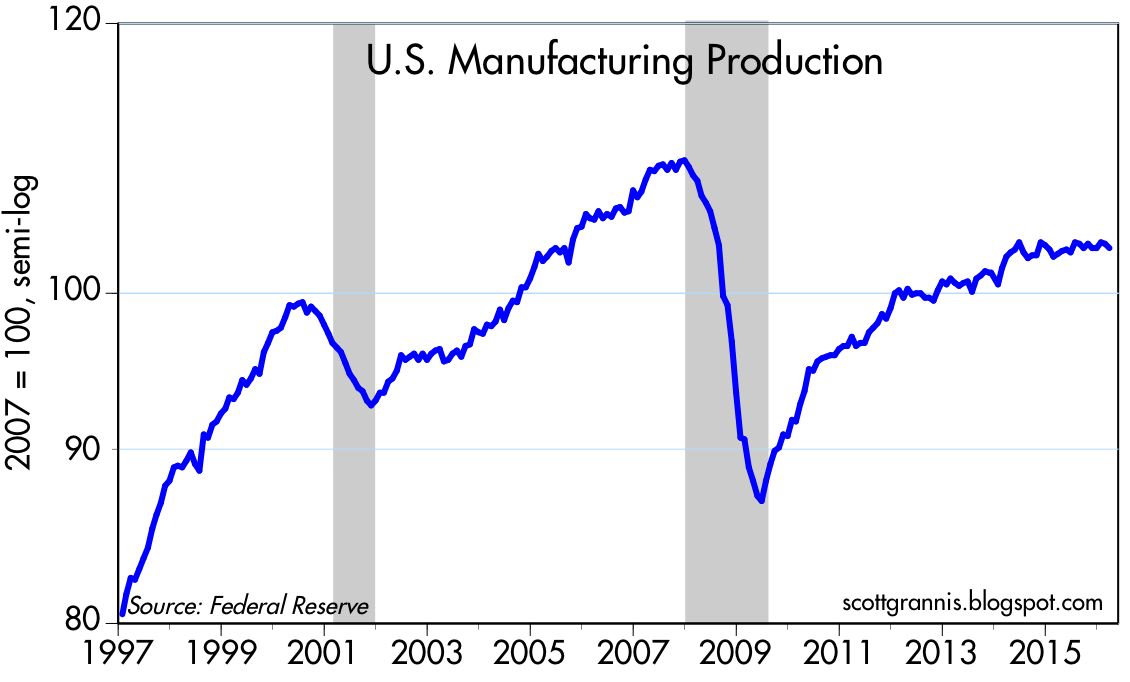

Industrial production and manufacturing in general have been the weakest sectors of the economy in recent years. Industrial production has been declining for almost 18 months now, but the lion's share of that decline can be traced back to the huge reduction in oil-related activities, which in turn are a logical response to plunging oil prices. As the next chart shows, manufacturing production has been flat for the past 18 months. Most of that weakness undoubtedly stems from declining production of energy-related equipment. Outside of the energy industry, life goes on in a relatively normal fashion, but with the under-appreciated boon that cheap energy represents to the vast majority of consumers.

Both the services and the manufacturing ISM indices confirmed that activity picked up towards the end of the first quarter, all but erasing the earlier slump. This likely means that the economy is back on the 2% growth track that has prevailed for the duration of the current business cycle expansion.

The employment subindex is once again back above 50, but only reflects modest improvement in employment going forward.

The U.S. and Eurozone economies have been tracking each other for the past 3-4 years, with both growing moderately.

The chart above compares the growth of prices in the service, non-durable, and durable goods sectors. Since 71% of the US workforce is employed in the private service sector, and since the cost of services is largely determined by wages, we can infer that the vast majority of the US workforce has been enjoying very healthy wage gains relative to durable goods prices. Service sector prices have been increasing at a modest 2% annual rate for the past several years, but they have increased two and a half times faster than durable goods prices since 1995 (which happens to mark the start of China's huge export boom).

This is equivalent to saying that an hour's worth of work in the service sector buys 2.5 times as much in the way of durable goods as it did in 1995. We can lament the tepid growth in median incomes over the past few decades, but this significantly understates the gains in workers' purchasing power for durable goods. Practically anyone who works these days is able to afford a smartphone, a device that replaces goods that would have cost a small fortune just 20 years ago. Let's not lose our perspective: things could be a lot better, but they could also be a lot worse.

Industrial production and manufacturing in general have been the weakest sectors of the economy in recent years. Industrial production has been declining for almost 18 months now, but the lion's share of that decline can be traced back to the huge reduction in oil-related activities, which in turn are a logical response to plunging oil prices. As the next chart shows, manufacturing production has been flat for the past 18 months. Most of that weakness undoubtedly stems from declining production of energy-related equipment. Outside of the energy industry, life goes on in a relatively normal fashion, but with the under-appreciated boon that cheap energy represents to the vast majority of consumers.

Monday, May 2, 2016

Still more encouraging developments

Markets continue to recover from the growth scare that set in beginning around the end of last year. Oil prices were plunging, creditors feared a wave of defaults, commodity prices were plunging, China was thought to be on the verge of a huge slowdown, and central banks appeared powerless to avoid another recession. What a difference a few months make. "Avoiding a recession is all it takes" has been a recurring theme of this blog for more than three years, and it's still relevant. Here are some more charts which suggest that instead of tipping over into a recession, the economy is more likely picking up a bit. Growth is still slow, but slow growth is a lot better than a recession, especially when cash yields almost nothing.

Here are some more charts updated with recent statistics that present an encouraging picture:

The chart above shows the price of crude oil futures. Oil prices are no longer declining and have instead rebounded over 70% from their February lows.

Construction spending in March was up 8% from year-ago levels, and has been exceeding expectations in recent months.

Industrial metals prices are up over 25% in the past three months, a good sign that global manufacturing activity is improving.

It's ironic that radically cheaper energy prices in the past year or so have been seen by many to be a source of concern (because they threaten the health of energy producers), when they have been a boon to consumers everywhere. As the chart above shows, energy has never been a smaller part of consumers' budgets than it was last March (3.67%). High and rising energy prices have tended to precede recessions, and falling energy prices have tended to coincide with periods of very healthy economic growth (e.g., the mid-1980s). This is not an ironclad rule, but it's hard to see a recession developing when energy—an essential ingredient to all economic activity—becomes very cheap.

UPDATE: And here is the current menu of yields available on different types of assets:

The chart below shows the difference between the earnings yield on equities (i.e., after-tax profits per share) and the yield on 10-yr Treasuries. Note that the current equity risk premium (i.e., what you would earn if corporate profits were to continue at the same level relative to share prices and corporations paid out all profits in the form of dividends) is still quite a bit higher than its long-term average. You don't often get the chance to pick up so much extra yield on equities. The explanation for why this is so high today is that investors don't believe that corporations will be able to sustain their current level of profitability. In other words, bad news is still priced in:

Here are some more charts updated with recent statistics that present an encouraging picture:

The April ISM manufacturing index was a bit lower than expectations (50.8 vs. 51.4), but it is still at levels which are consistent with overall growth in the economy of 2% or better. It's rebounded nicely from the lows of just a few months ago.

The export orders index has also rebounded nicely, and that's especially encouraging since the market has been very worried about slowdowns in overseas markets.

The chart above shows the price of crude oil futures. Oil prices are no longer declining and have instead rebounded over 70% from their February lows.

With the plunge in oil prices a thing of the past, we see that prices of things other than oil are still rising. (The Core CPI has been rising at an annualized rate of 2% or so for many years.) A majority of companies in April reported paying higher prices, as the chart above shows. Deflation risk is vanishing.

Construction spending in March was up 8% from year-ago levels, and has been exceeding expectations in recent months.

Industrial metals prices are up over 25% in the past three months, a good sign that global manufacturing activity is improving.

Bank lending to small and medium-size businesses has been booming for the past five years. C&I Loans are up 11% in the past year, and have surged at an annualized rate of almost 20% in the past three months. This is an excellent indicator of rising confidence, since banks are evidently more willing to lend and businesses are more willing to borrow. Total Bank Credit outstanding has been rising at a 7-8% annual rate of late as lending has increased by $767 billion in the past year (for perspective, that's equivalent to 4.2% of GDP).

It's ironic that radically cheaper energy prices in the past year or so have been seen by many to be a source of concern (because they threaten the health of energy producers), when they have been a boon to consumers everywhere. As the chart above shows, energy has never been a smaller part of consumers' budgets than it was last March (3.67%). High and rising energy prices have tended to precede recessions, and falling energy prices have tended to coincide with periods of very healthy economic growth (e.g., the mid-1980s). This is not an ironclad rule, but it's hard to see a recession developing when energy—an essential ingredient to all economic activity—becomes very cheap.

UPDATE: And here is the current menu of yields available on different types of assets:

The chart below shows the difference between the earnings yield on equities (i.e., after-tax profits per share) and the yield on 10-yr Treasuries. Note that the current equity risk premium (i.e., what you would earn if corporate profits were to continue at the same level relative to share prices and corporations paid out all profits in the form of dividends) is still quite a bit higher than its long-term average. You don't often get the chance to pick up so much extra yield on equities. The explanation for why this is so high today is that investors don't believe that corporations will be able to sustain their current level of profitability. In other words, bad news is still priced in:

Subscribe to:

Posts (Atom)